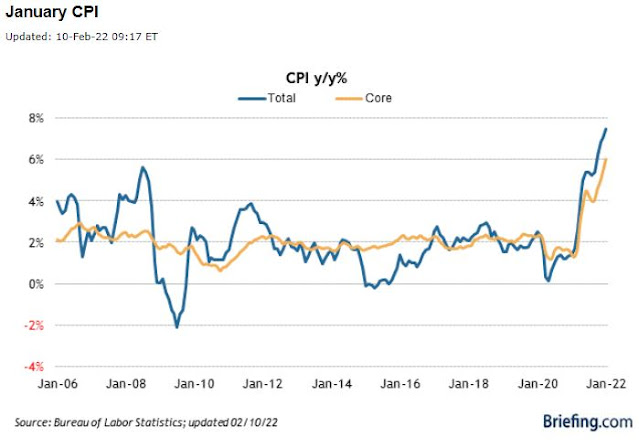

The Consumer Price Index (CPI) rose 0.6% month-over-month (m/m) in January, above the Bloomberg consensus estimate of a 0.4% increase, and following December's upwardly-revised 0.6% gain. The core rate, which strips out food and energy, also increased 0.6% m/m, topping forecasts of a 0.5% gain, and matching December's unadjusted rise. Compared to last year, prices were 7.5% higher for the headline rate—the fastest pace since 1982—above estimates of a 7.3% increase and an acceleration from the prior month's 7.0% rise. The core rate was up 6.0% y/y, above projections of a 5.9% increase, and following December's unrevised 5.5% rise.

Weekly initial jobless claims came in at a level of 223,000 for the week ended February 5, versus estimates calling for 230,000, and down from the prior week's upwardly-revised 239,000 level. The four-week moving average declined by 2,000 to 253,250, and continuing claims for the week ended January 29 was unchanged at 1,621,000, versus of estimates of 1,615,000. The four-week moving average of continuing claims rose by 16,500 to 1,634,500.

Treasuries are falling following the inflation data, with the yield on the 2-year note jumping 12 basis points (bps) to 1.46%, while the yields on the 10-year note and the 30-year bond are rising 5 bps to 1.98% and 2.28%, respectively.

Earnings continue to support market values

In the end, earnings drive market values. As Q4 earnings season continues to roll on, of the 342 companies that have reported results in the S&P 500, 68.82% have topped revenue forecasts, while 76.54% have bested earnings expectations, per data compiled by Bloomberg. Compared to last year, revenue growth is on pace to be up nearly 16.36% and earnings expansion is on track for about 26.87%.

Comments

Post a Comment

Thanks for the comment. Will get back to you as soon as convenient, if necessary.